NASA’s successful Artemis II launch on April 1, 2026, marks an important near-term win for the program, even as the agency moves away from the Lunar Gateway and toward a surface-first lunar strategy. The juxtaposition is striking: one pillar of Artemis has just been validated in flight, while another has been effectively set aside.

This article analyzes the drivers behind NASA’s decision (on March 24th) to cancel the Lunar Gateway, and its implications for the Artemis program, international partners, and the commercial ecosystem, highlighting what lies ahead: increased reliance on commercial actors, redefined partnerships, intensified competition with China, and growing uncertainty around long-term funding and program coherence.

What is Happening: A Structural Shift in NASA’s Lunar Strategy

As anticipated in Novaspace’s Prospects for Space Exploration (released in April 2025), the Lunar Gateway has now been effectively cancelled. Initially viewed as a central element of NASA lunar architecture, its cancellation, on March 24th 2026, marks a material shift in the Artemis Program. According to current policy direction and budget proposals, the agency plans to repurpose selected Gateway technologies while redirecting funding toward the development of a sustained lunar surface presence, including infrastructure for a Moon base.

This decision is part of a broader simplification of the Artemis architecture, aimed at reducing complexity and accelerating deployment timelines. By removing the intermediate orbital layer, NASA is moving toward more direct mission profiles between Earth and the lunar surface. In parallel, the agency is reinforcing a shift toward commercially supported transportation and logistics, with the objective of increasing mission cadence and reducing reliance on government-owned systems. This includes the expansion of the Commercial Lunar Payload Services (CLPS) framework to support more frequent cargo deliveries, as well as a reassessment of the long-term role of the Space Launch System. Beyond Artemis V, NASA has indicated its intention to rely on multiple commercial lunar transportation providers, marking a transition toward a more diversified and competitive transport architecture.

Several factors underpin this strategic shift:

- Schedule pressure across the Artemis Program has increased, with delays affecting key elements such as the Human Landing System and mission timelines. The Gateway, whose first elements were planned for launch around 2027 and operational use around 2028, was not required for the initial crewed landing missions, reducing its short-term criticality.

- Budget and portfolio constraints are driving prioritization toward programs with more immediate operational returns. Gateway represented a multi-phase infrastructure investment with benefits materializing over the long term, whereas surface systems enable earlier deployment of capabilities and more visible outcomes.

- The decision reflects a geopolitical logic. The United States is seeking to secure a leading position in lunar surface operations in the context of intensifying competition with China. From this perspective, surface infrastructure offers both faster deployment and stronger strategic signalling than an orbital platform.

Taken together, these elements point to a clear change in priority: from orbital infrastructure designed to provide long-term flexibility and system integration, to surface infrastructure aimed at delivering near-term operational presence and geopolitical visibility. This shift also confirms a broader transition within NASA’s exploration strategy, from infrastructure-led architectures toward operations-driven and commercially enabled mission models.

What Was the Gateway Program About? A Central but Contested Architectural Layer

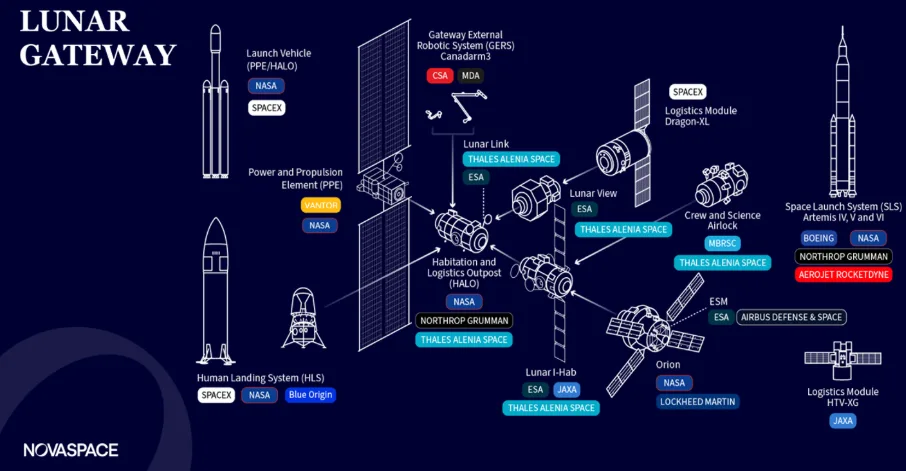

The Lunar Gateway was conceived as a human-tended, multi-purpose outpost in lunar orbit, developed as a cornerstone of the Artemis Program. Led by NASA, and designed in collaboration with other international space agencies (ESA, JAXA, CSA, and the UAE) and commercial players, the Gateway was intended to support sustained lunar operations, serving as a staging node for crewed and robotic missions, a logistics hub, and a platform for deep-space science and technology demonstration. It also played a strategic role as a bridge architecture, linking short-term lunar exploration with longer-term ambitions toward Mars.

Lunar Gateway Key Characteristics

Gateway was designed as a modular station in near-rectilinear halo orbit (NRHO), enabling continuous visibility of the lunar south pole and efficient access to the surface. Its core elements included the Power and Propulsion Element (PPE), the HALO habitation module, and additional international contributions such as habitation, logistics, robotics, and airlock systems. Had it been completed in the early 2030s, the station was expected to reach 10–20% of the scale of the International Space Station, accommodating crews of up to four astronauts for missions of one to three months, and supporting both surface operations and communications relay.

The initial program followed a phased development timeline:

Financially, Gateway represented a mid-scale infrastructure investment within Artemis. NASA’s initial investments accounted for about $4.4 billion1, spent between 2019 and 2025, with additional billions projected through the end of the decade to reach initial operational capability. However, its value proposition was increasingly reassessed in light of evolving budget priorities. In the context of NASA’s FY2025 and FY2026 proposals, the agency signaled a shift toward reallocating resources to a significantly larger ~$20 billion lunar surface infrastructure program. This transition reflects a reprioritization toward investments more directly aligned with the objective of establishing a sustained human presence on the Moon. In this context, Gateway’s contribution, while structurally important, was perceived as less immediately instrumental in achieving that objective, making it more difficult to justify within a constrained and politically scrutinized budget environment.

Partners Involved: Alliance Disruption and Programmatic Consequences

The cancellation of the Lunar Gateway introduces a significant alliance-management challenge for NASA and the Artemis Program. Gateway was not only a technical component, but also a central framework for international participation, structuring contributions from multiple partners and underpinning broader cooperation under the Artemis Accords. Its removal therefore requires a renegotiation of both institutional commitments and industrial contracts, with implications across a wide network of stakeholders. NASA has indicated that Artemis prime contractors alone involve more than 2,700 suppliers across 47 U.S. states, highlighting the scale of the industrial ecosystem affected.

Among U.S. suppliers, key contributors include Boeing, Lockheed Martin, Northrop Grumman, Blue Origin, and Maxar Technologies, which are responsible for major elements such as habitation modules, propulsion systems, and launch capabilities.

International suppliers were part of the Gateway program, notably:

- The European Space Agency (ESA) is the most exposed: Its contributions, including the Lunar I-Hab module, Lunar View, and Lunar Link, were specifically designed for Gateway’s architecture. The cancellation raises uncertainties regarding the redeployment of these investments and assets, as well as the broader balance of transatlantic cooperation in exploration. ESA plans to submit a plan on how to move forward in June during its next Council.

Another key issue lies in human spaceflight access. ESA’s participation in Gateway was expected to translate into guaranteed astronaut flight opportunities within the Artemis program. With this framework now uncertain, Europe’s visibility on future crewed missions beyond low Earth orbit becomes significantly reduced.

- Japan Aerospace Exploration Agency (JAXA) faces a more mixed situation. Its planned contributions to Gateway, such as life support systems, batteries, and logistics through the HTV-XG vehicle, are directly affected. However, Japan retains a significant role in surface operations, notably through the pressurized lunar rover agreement signed with NASA in 2024, partially mitigating the impact on its overall lunar strategy.

- For the Canadian Space Agency, exposure is concentrated on robotics and associated political returns. The Canadarm3 system was a flagship contribution to Gateway, tied to agreements on astronaut flights and long-term participation. The program’s cancellation therefore, raises questions about the preservation of these commitments and the repositioning of Canada’s role within Artemis.

- The Mohammed Bin Rashid Space Centre in the United Arab Emirates is particularly affected. Its planned airlock module was highly specific to Gateway’s orbital configuration, making repurposing more complex than for other contributions. This creates a potential mismatch between existing industrial developments and future program needs.

- Key international industrial contributors include Thales Alenia Space, which is responsible for critical Gateway modules such as ESPRIT and the I-Hab habitation module, as well as involvement in the Emirates airlock. Other major European partners include Airbus Defence and Space, which co-develops habitation systems, while Japan contributes through Mitsubishi Electric and other industrial actors supporting JAXA-led systems, and Canada through MDA, notably for the Canadarm3 robotic system.

Publicly disclosed contracts engaged for the Lunar Gateway program amount to $4.4 billion, financed by NASA, ESA, and CSA, while the value of remaining agreements has not been disclosed.

Beyond institutional and industrial considerations, the scientific community is likely to be one of the most impacted stakeholders. Gateway was intended to serve as a human-tended deep-space research platform, hosting payloads focused on radiation, heliophysics, and long-duration operations beyond low Earth orbit. Its cancellation removes a planned environment for sustained deep-space experimentation, potentially delaying or redistributing these scientific objectives.

Broader Implications: A Shift in Geopolitical and Industrial Dynamics

The cancellation of the Lunar Gateway extends beyond programmatic adjustments and reflects a broader repositioning of U.S. strategy in the global space landscape.

At its core, the shift toward a surface-first architecture reinforces the centrality of visible and sustained lunar presence as a marker of geopolitical leadership, particularly in the context of growing competition with China. China is advancing a parallel strategy through the planned International Lunar Research Station (ILRS), developed in partnership with Russia and other countries, which aims to establish a permanent robotic, and eventually human presence on the lunar surface in the 2030s, supported by infrastructure for energy, communications, and in-situ resource utilization. In this context, while Gateway was designed as an enabling orbital infrastructure, a sustained presence on the lunar surface provides stronger strategic signaling and aligns more directly with emerging concepts of operational presence and long-term foothold beyond Earth.

This transition also has implications for the multilateral governance model underpinning Artemis. Gateway functioned as a structural anchor for international participation, enabling a contribution-based framework similar to the International Space Station. Its cancellation weakens this model, shifting cooperation toward more bilateral or mission-specific arrangements, where roles are less clearly defined and potentially more flexible, but also less institutionalized.

The change in architecture is further reshaping the commercial space ecosystem. Under the Gateway-centered model, value creation was concentrated around orbital infrastructure, including station logistics, servicing, docking systems, and cislunar transport. The shift toward surface operations redirects demand toward lunar landers, cargo delivery, surface habitats, power systems, and in-situ resource utilization technologies. This transition is likely to reconfigure industrial opportunities, favoring actors positioned in surface logistics and operations, while reducing prospects for companies specialized in orbital station infrastructure.

Finally, the decision raises a broader question regarding U.S. credibility as a long-term program leader. Gateway represented a flagship international architecture with formal commitments from multiple partners. Its cancellation requires the United States to demonstrate that it can redefine a major exploration program without undermining coalition trust, by ensuring continuity of cooperation through alternative contributions and roles. The management of this transition will be critical in determining whether Artemis remains a stable framework for international collaboration or evolves into a more fluid, U.S.-centric model.

Key Takeways: What Comes Next?

- Expansion of the role of commercial actors

The transition away from Gateway and the reduced reliance on the Space Launch System point to a model increasingly based on commercial transportation, logistics, and surface systems. Unlike the Gateway architecture, largely structured around established prime contractors, this shift could open the field to a wider range of players, including smaller companies and startups, by creating more modular and mission-specific opportunities.

However, key uncertainties remain around whether commercial providers can deliver at the required scale, cadence, and cost, and whether this approach can support sustainable long-term exploration architectures or remain focused on near-term mission execution.

- Redefining of international partnerships

The removal of Gateway as a central coordination platform introduces uncertainty for international partners, whose contributions were structured around a stable, long-term architecture. Beyond immediate programmatic impacts, this raises broader questions about trust and reliability in U.S.-led frameworks, particularly in a context where many countries are increasingly prioritizing sovereign capabilities and reducing strategic dependence, already visible in defense and industrial policies. This could affect not only Artemis, but also future multilateral exploration initiatives, potentially accelerating a shift toward more fragmented or regionally aligned cooperation models. Countries such as India are advancing in human spaceflight and lunar missions, while actors like the United Arab Emirates, and increasingly Saudi Arabia, are stepping up their ambitions through partnerships and investments.

- Acceleration of geopolitical competition on the Moon

The focus on surface infrastructure reflects an emerging dynamic in which presence itself becomes strategic. In the absence of clearly established economic returns, lunar competition is currently driven as much by visibility, influence, and standard-setting as by immediate utilization. This raises the question of whether the Moon will evolve into a domain of operational and economic activity (e.g., resource extraction, infrastructure deployment), or remain primarily a symbolic and geopolitical frontier, where actors seek to avoid strategic absence rather than exploit concrete value.

- Reallocation of budgets and financing priorities

The proposed shift toward a ~$20 billion lunar surface initiative introduces significant funding uncertainty. It remains unclear whether NASA will secure the full budget required, particularly in a constrained fiscal environment. At the same time, the program must address the reallocation of multiple billions already committed to Gateway, including the justification of sunk costs and the repurposing of existing hardware and contracts. This raises broader questions about program continuity, cost efficiency, and political support, and whether future exploration initiatives will need to demonstrate faster and more tangible returns to secure sustained funding.

***

These insights are drawn from our Space Exploration Report, which provides a comprehensive economic and strategic assessment of the global exploration sector. Covering key domains including low Earth orbit human spaceflight, lunar and Mars exploration, and deep space science, the report analyzes government programs, commercial initiatives, and emerging entrants worldwide. It combines detailed forecasts of missions and funding with an in-depth assessment of the evolving exploration ecosystem, across transportation, infrastructure, and resource utilization, to identify the key trends and structural shifts shaping the future of space exploration.