Global government space programs are entering a new phase of transformation. After a decade of sustained expansion, 2025 marks a record level of spending, stabilizing into a temporary plateau that reflects a strategic recalibration ahead of a projected surge from 2026 onward. This transition signals a shift in priorities, with governments increasingly focusing on operational impact, resilience, and strategic autonomy. Three structural shifts define this evolution: the prioritization of high-impact capabilities, the emergence of a more distributed global landscape, and the rise of integrated, hybrid space models.

Shifting from Expansion to Strategic Prioritization

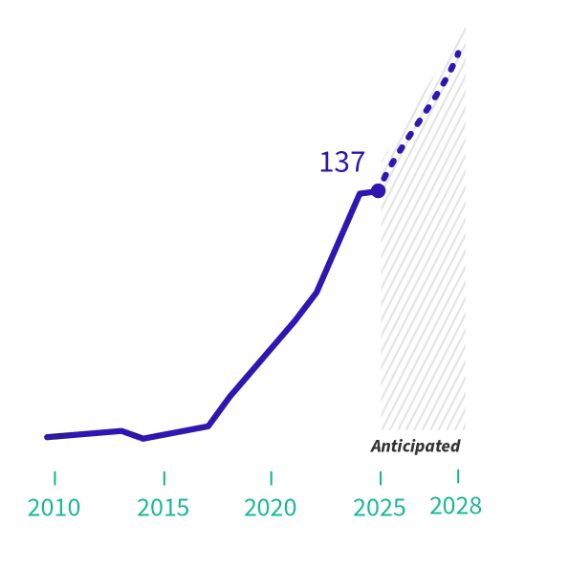

After more than a decade of sustained growth, government space programs reached a new high in 2025, with growth stabilizing into a temporary but structurally necessary plateau. Global public space spending reached approximately $137 billion in 2025, as governments pause to reassess priorities and absorb recent program expansions. This phase is expected to be short-lived, with spending projected to increase sharply from 2026 onward, by over 20% in one year, driven primarily by defense programs and large-scale infrastructure initiatives.

World total government space expenditures (2010-2028), in billion USD

This transition reflects a shift in spending composition, governments are prioritizing programs that deliver near-term operational impact, particularly in areas linked to national security and sovereignty.

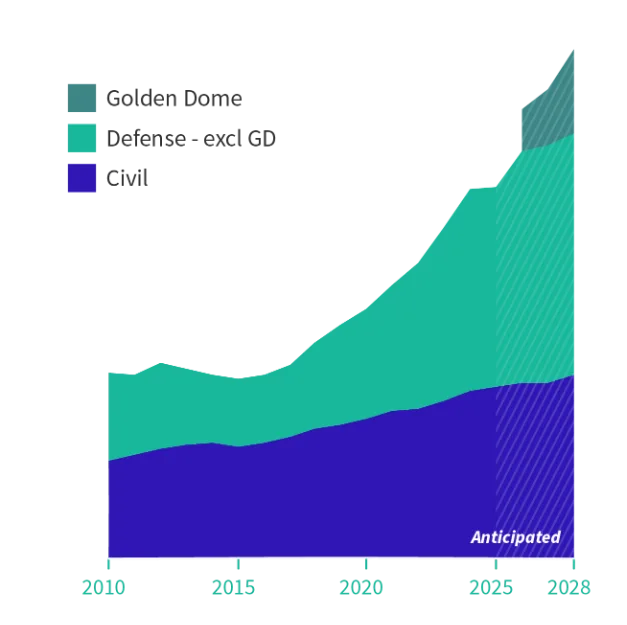

Defense is now the main structuring force behind public space budgets, with space increasingly treated as critical infrastructure whose disruption could directly affect military operations and national resilience. This shift is reflected in the rapid growth of space security and early warning applications, supported by the development of integrated orbital architectures combining missile warning systems, proliferated LEO constellations, and resilient multi-layer communication networks. At the same time, the rising deployment of reconnaissance and inspection satellites underscores the increasingly contested nature of the space domain.

Public Civil and Defense Space Expenditures (2010-2028), in relative investment scale

Growth across other applications is more differentiated. Telecommunications, Earth observation, and Navigation continue to expand steadily, supported by both civil and defense demand. Human spaceflight is also gaining renewed momentum, driven by lunar ambitions and the transition toward post-ISS architectures. By contrast, launch remains more cyclical, reflecting procurement timing and the growing reliance on commercial services, even as access to space remains a strategic priority and continues to support investment in next-generation and reusable launch systems.

Finally, major exploration programs are under greater scrutiny. Delays and cost pressures within the Artemis program, as well as the cancellation of the Lunar Gateway, illustrate a shift toward simplified architectures and faster operational returns, prioritizing surface capabilities over long-term infrastructure.

National Strategic Differentiation

The global space ecosystem is becoming more distributed, but more importantly, it is evolving toward a landscape where countries are leveraging space capabilities in increasingly differentiated ways aligned with national priorities. While the United States remains dominant in overall spending, the relative rise of other actors reflects not just growth in budgets, but a diversification in how space is used and positioned within national strategies.

Top 5 fastest-growing countries by government spending (>$30 million)

This differentiation is particularly visible in Asia, the fastest-growing region in terms of space investments, where countries are pursuing distinct trajectories. China continues to invest across the full spectrum, combining human spaceflight, lunar exploration, and large-scale constellations to support both geopolitical positioning and long-term technological leadership. In contrast, India emphasizes cost-efficient exploration and launch capabilities, positioning itself as a competitive provider while gradually expanding defense applications. Japan focuses on dual-use technologies and strategic partnerships, including contributions to international programs and investments through its Space Strategy Fund.

Other countries are adopting more targeted and operational approaches. South Korea is developing sovereign launch capabilities and Earth observation systems, while Australia prioritizes space domain awareness and communications infrastructure aligned with defense and regional security objectives.

Space is increasingly used as a tool for economic positioning and technological development. In the Middle East, countries such as United Arab Emirates combine high-visibility missions, including lunar and planetary exploration, with investments in downstream applications and industrial partnerships, while Saudi Arabia is expanding its presence in communications and space services.

In other regions, space programs are often driven by immediate socio-economic needs rather than strategic autonomy. Countries such as Cambodia or Philippines focus on Earth observation and satellite data to support agriculture, disaster management, and environmental monitoring, relying on partnerships rather than sovereign infrastructure.

While global rankings remain relatively stable in 2025, underlying trajectories suggest a gradual shift in influence. Emerging investments, such as Germany’s defense-space expansion or South Korea’s launcher roadmap, indicate that future competition will be shaped less by overall spending than by the ability to align space capabilities with clearly defined national objectives.

The Rise of Hybrid Space Models: Civil, Defense, and Commercial Convergence

Government space programs are increasingly evolving toward hybrid models, where civil, defense, and commercial capabilities are no longer developed in isolation but integrated into coherent operational ecosystems.

A first dimension of this shift is the blurring of boundaries between civil and defense space activities. Many systems are now inherently dual-use, with civil infrastructure supporting security functions and vice versa.

At the same time, governments are making greater use of commercial capabilities, shifting from ownership-driven models toward more flexible procurement strategies. Rather than systematically developing sovereign systems, public actors are increasingly relying on private providers for launch services, satellite data, and even human spaceflight. This is evident in the growing use of commercial Earth observation data for public missions, as well as in exploration, where programs such as Artemis Program incorporate commercially developed landers and services. This trend is further institutionalized through national and international frameworks, even on the defense side, including the growing role of commercial providers in U.S. defense procurement, China’s structured integration of commercial actors, and NATO’s formal recognition of commercial space assets within collective defense planning.

Space systems are shifting toward architecture-based approaches, where governments design integrated systems rather than standalone missions. Constellations, data infrastructures, and multi-orbit networks are increasingly developed as interconnected assets, supporting applications across defense, communications, navigation, and Earth observation. Proliferated LEO constellations and layered architectures are becoming central to this model, enabling redundancy, resilience, and operational flexibility in an increasingly contested domain. At the same time, value creation is progressively moving downstream, toward data processing, analytics, and service delivery, reflecting the growing importance of information superiority in both civil and defense contexts.

What Comes Next: from space programs to space power

These insights are drawn from our Government Space Report, which provides a comprehensive analysis of global public space expenditures, strategic priorities, and program developments across more than 90 countries. The report combines quantitative data with in-depth policy and market analysis to track how government space investments are evolving and shaping the broader space ecosystem. It also offers detailed breakdowns of key figures, including budgets by country, region, and application, providing a granular view of global space investment dynamics.