Under financial strain and strong competition from SpaceX Transporter, commercial small launchers are now racing to heavy next-generation launchers they hope will open on larger markets. Indeed, after $9 billion raised in private funding since 2017, commercial small launchers hold a combined backlog of only $400 million in launch contracts and besides Rocket Lab, the next most advanced companies have launched only once or twice so far.

Thus, it seems the market is rediscovering the lessons learnt from SpaceX’s Falcon 1 twenty years ago, with small launch operators not content of the smallsat dedicated launch market and moving straight to heavy follow-ons. This time though, there are more contenders, the demand landscape is rapidly changing, and all western launch providers face intense competition from SpaceX’s now-heavy launchers and upcoming Starship.

With high price and low frequency small launchers miss out on most of the market

With a high price per kg (up to 5 or 10 times higher than entry price on SpaceX Transporter), and low launch rates overall, commercial small launchers find mostly niche users such as government technology demonstrators, bring-into-use satellites, or small cubesat constellations with specific injection needs. Fast time-to-orbit and responsiveness for defense users has often been marketed as their strong suit, making up for high price, but so far their reactivity (time from contracting to orbit) stands at over one year for most providers.

Meanwhile small launchers miss out on most of the constellation launch demand (making up 82% of satellites to be launched within the next decade), as constellation operators are more cost-constrained and seek rapid deployment, which can only be achieved by batch or rideshare launches on heavy vehicles (outside of cubesat constellations). As of 2023, constellation satellites manifested on small launchers with commercial providers accounted for only 4 tons of launch mass (almost entirely cubesats), out of a total 2 300 tons for all launcher types.

Due to the combination of reduced payload capacity and the incompressible costs of the launch industry, resulting in thin margins, achieving high launch rates is key for most small launcher and the only way to attract more constellation customers. But ramping up operations beyond first launch on limited equity funding has proven very challenging so far. Since 2023, one high profile small launch provider has gone bankrupt and another has left NASDAQ with a fraction of its valuation. Even Rocket Lab, which was founded 18 years ago and first launched Electron 7 years ago, holds a record of 9 launches per year (excluding Chinese government solid launchers).

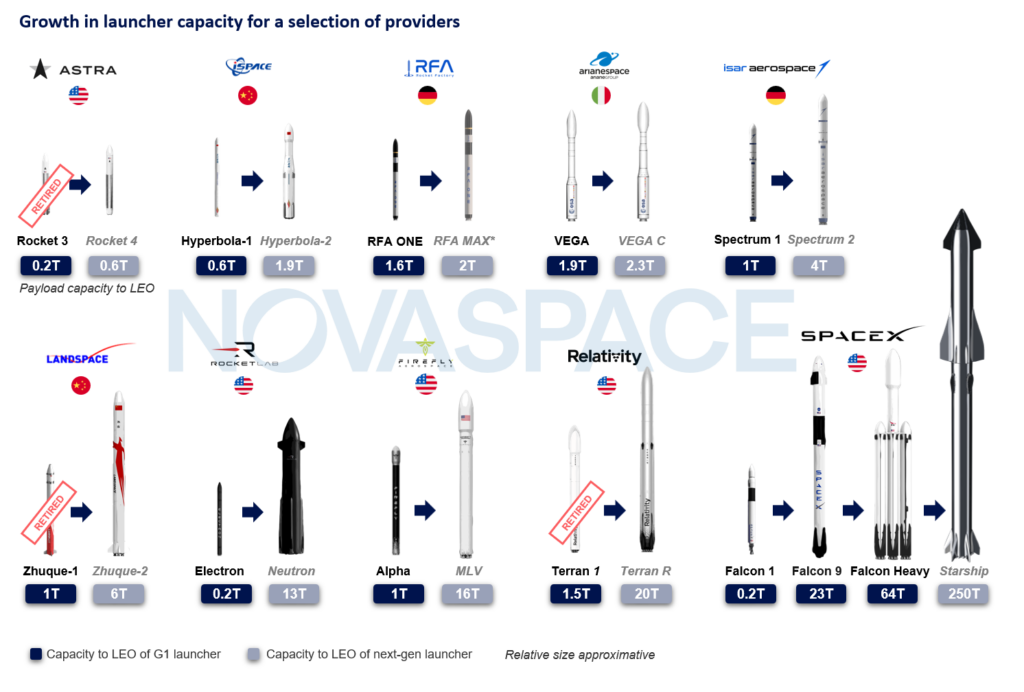

Small launch providers racing to heavy follow-ons – again.

Hence, almost all emerging small launch companies are now planning heavier follow-on vehicles opening on larger markets, trying to move away from a high rate, low margin/launch economic model. However, with most equity funding raised already spent in small first-generation launchers, funding of the heavy follow-on is often uncertain. Next-gen heavy launchers will be more expensive and longer to develop, asking more from private investors who often joined out of fear of missing out, and have yet to see a return on their initial investments.

Thus, present commercial small launchers are following the path SpaceX took in the late 2000s, abandoning Falcon 1 and all plans for small launch after 5 launches and moving on to the heavy Falcon 9 which would open on much larger markets (and was almost entirely financed by NASA’s commercial Human spaceflight programs). SpaceX’s Transporter rideshare opportunities are now the biggest challenge to all small launch providers, having launched 81% of small satellite globally (not counting Starlink and chinese satellites) from 2019 to 2023.

Small launch providers diversifying across the board

Meanwhile, indicating pressure on their core business, many providers are diversifying into other space businesses. Rocket Lab for instance, the most advanced small launch provider, in 2023 stemmed two-thirds of its revenue from satellite manufacturing activities. Other providers have announced diversifications in space systems or subsystems, such as satellite propulsion for Astra, and satellite systems or subsystems for Phantom Space and Gilmour Space.

Another area of interest is smallsat Last Mile Delivery (LMD) with Orbital transfer Vehicles, an additional mobility service acting as demand relay for its core launch business. Firefly is to introduce its OTV Elytra, with strong heritage from its acquisition of Spaceflight in 2023. Skyrora too is planning an OTV while Launcher Space, initially a small launch company, has pivoted entirely into LMD, discontinuing its launcher program when acquired by VAST. Even Blue Origin, though not a small launch operator, is now planning an OTV.

Lessons for the launch market

So far, it seems no one has fully cracked the code for sustainable commercial small launch. Small launch frequency is low, with about a year between a provider’s any two launches (except for Rocket Lab and Chinese government solid launchers), and specific prices per kg are typically over 10 times the Transporter entry price, leaving small launchers with mostly niche users.

Almost 20 years after Falcon 1’s first launch, the market is reminded that small satellites do not necessarily call for small launchers, and most of the emerging providers face doubts about funding their heavy successors. Yet, with SpaceX’s growing monopoly on the heavy launch market and near-term bottleneck on heavy launch, many users are increasingly keen on seeing alternative providers, many of which were directly inspired by it and instigated in its wake. Still, it has yet to be seen if SpaceX’s model, combining the largest, self-funded satellite constellation demand, reusability and extensive US government demand, can be replicated.

Want to learn more about trends in the launch market? Check out Novaspace’s Launcher Database, cataloging over 800 launchers, existing or proposed, listing operator and manufacturer, payload capacity and pricing.