NASA’s Commercial Lunar Payload Services (CLPS) program is entering a fundamentally new chapter. The shift is not about delivering more science packages to the Moon; it is about building a permanent surface presence. That ambition demands a level of logistics cadence, industrial capacity, and technical maturity that CLPS 1.0 was never designed to provide. For commercial providers, suppliers, and investors across the space sector, understanding where this program is headed, and what it will require, is now a strategic imperative.

CLPS 1.0: What the First Phase Achieved and Where it Fell Short

The first phase of CLPS demonstrated that commercial lunar delivery was feasible. It generated market momentum and brought multiple providers into a nascent but credible industry.

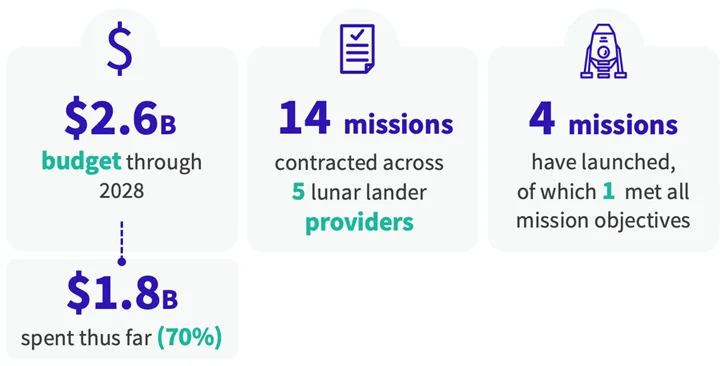

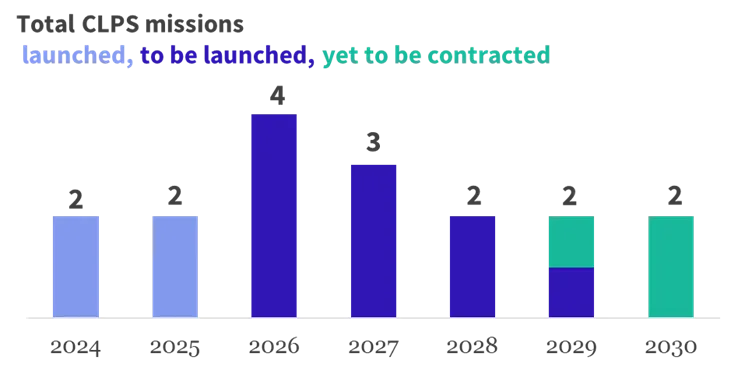

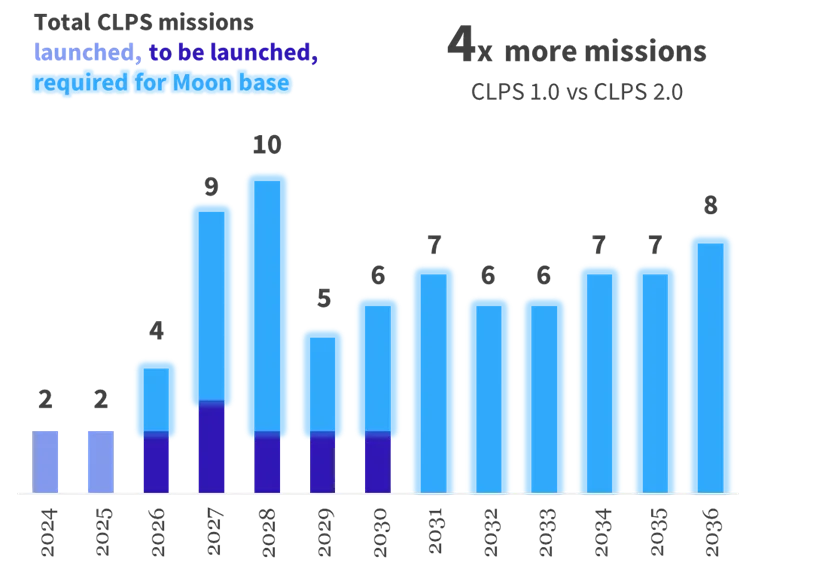

Fourteen missions have been contracted under CLPS 1.0, with three additional missions announced but not yet formally contracted, bringing the total program count to 17. Four missions have launched since 2024, supported by a budget of $2.6 billion over a ten-year contracting period ending in 2028, of which roughly 70% has already been allocated[1].

By any measure, this is a meaningful program. At the same time, the program has exposed the current limits of the market. Of the missions launched so far, only one fully achieved all mission objectives. Launch cadence has remained limited to roughly two missions per year, while average schedule delays have reached 14 months. Those results do not invalidate the program, but they do define the baseline from which the next phase must grow.

CLPS Program Overview to Date

CLPS 2.0: A Fourfold Increase in Scale with Tighter Economics

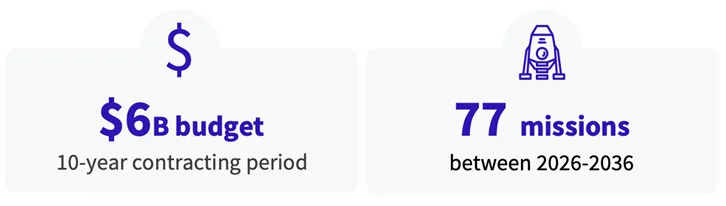

The contrast with CLPS 2.0 is stark. NASA’s roadmap to establishing a permanent lunar base requires no fewer than 77 lander missions over the coming decade[2]. A portion of these will fall within the current CLPS phase; the majority are allocated to CLPS 2.0. Compared to the roughly 15 lunar lander missions conducted globally over the prior decade[3], that represents a fivefold increase. Compared to CLPS 1.0 alone, it is roughly four times the volume.

This is not an incremental change. It is a structural transformation of the commercial lunar delivery market.

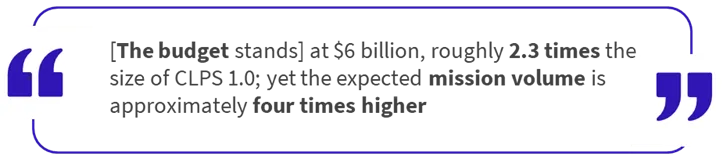

As for the budget, it stands at $6 billion, roughly 2.3 times the size of CLPS 1.0; yet the expected mission volume is approximately four times higher[4]. The math is just as revealing at the mission level: under CLPS 1.0, the average cost of delivering a lander to the Moon has been about $129 million per mission; under CLPS 2.0, that figure falls closer to $91 million[5]. The larger budget does, however, create one structural advantage: the potential for block buys, which introduce planning predictability. For providers, that predictability is a prerequisite for investing in production capacity, supply chain development, and long-term capability building.

For industry, that is both the opportunity and the catch. Four to five times more missions will not be achieved by executing the current model slightly better. It will require a different operating model built on repeatability, standardization, and industrial capacity. The headline for CLPS 2.0 may be cadence, but the deeper story is transformation.

Where CLPS 2.0 is Headed

Four Signals Already Shaping CLPS 2.0

The Draft RFP[6] and NASA’s Moon base roadmap[7] contain several provisions with direct strategic implications for commercial lunar lander providers.

(1) Higher Performance Expectations

CLPS 2.0 raises the bar substantially. Missions will involve heavier cargo, longer surface durations, and more demanding operational profiles. NASA’s roadmap indicates that by 2031, small-class landers (the backbone of CLPS 1.0) will no longer be sufficient. Medium- and heavy-class vehicles will define the standard. Cargo and payload mass projections reinforce this trajectory: approximately 3 tonnes will be delivered under CLPS 1.0, rising to roughly 60 tonnes between 2029 and 2033, and to around 150 tonnes between 2033 and 2036[8].

The implication is straightforward: industry will need to develop, qualify, and finance new capabilities before those capabilities begin reducing risk. That creates a demanding transition period in which technical ambition rises ahead of operational maturity.

(2) Tightened Domestic Sourcing Threshold

A second major signal is less visible but potentially just as consequential. The draft RFP proposes increasing the domestic sourcing threshold from 65% through 2028 to 75% by 2029[9]. Compliance would not be symbolic; it would be a material condition of payment and contract eligibility.

This may appear to be a procurement detail, but its effects are strategic. Higher domestic content requirements could drive component requalification, supply chain redesign, and greater dependence on a still-limited base of domestic suppliers. In other words, this sourcing policy could become a bottleneck to cadence.

For providers, the issue is not just compliance. It is competitiveness, schedule risk, and cost structure.

(3) Push For Standardization

Among the more strategically significant signals in the Draft RFP is NASA’s explicit request for contractor input on common interface standards: mechanical and electrical connections, mounting configurations, command interfaces, mass range definitions, and other mission elements. That is a direct response to one of the clearest lessons from CLPS 1.0: bespoke mission accommodations are expensive. They add complexity, extend schedules, and force providers into repeated non-recurring engineering. Standardization offers a different path; one that enables repeatable production, compresses redesign cycles, and creates conditions for meaningful cost reduction at scale.

(4) Increased NASA Oversight

This last element slightly contradicts the previous as it could reduce the scalability of CLPS 2.0.

Indeed, the Draft RFP signals a move toward closer agency involvement in high-stakes missions: more detailed reporting, deeper technical knowledge sharing, and in some cases embedded NASA engineers[10]. The rationale is understandable, but historical evidence from CLPS 1.0 suggests that heightened hands-on oversight has correlated with higher mission costs and schedule pressure. The difference this time is that NASA is openly acknowledging this tension and inviting industry input on how tighter collaboration should be structured. That is constructive, but only if the governance model is disciplined. If oversight increases, NASA project management must operate as an enabler of execution, not a source of additional friction. Otherwise, the burden of operating with agility in an environment with a low risk tolerance will be borne solely by industry.

Conclusion: An Industry-Wide Opportunity, Not A Single-Provider Race

CLPS 2.0 asks industry to deliver more missions at lower unit cost while simultaneously absorbing heavier technical requirements, tighter sourcing rules, and closer government oversight. That combination can work, but only if standardization delivers real savings, procurement creates predictability, and suppliers can invest ahead of demand.

What is equally clear is that no single provider can meet this demand alone. The next phase of CLPS is, at its core, a major opportunity. The companies that establish repeatable lunar logistics operations, anchor interface standards, and build resilient domestic supply chains in the years ahead will define the architecture of the commercial lunar surface market for the decade that follows.

[1] According to Novaspace estimations.

[2] National Aeronautics and Space Administration (NASA), “Building the Moon base,” PDF, accessed April 20, 2026, https://www.nasa.gov/wp-content/uploads/2026/03/2-building-the-moon-base.pdf.

[3] According to Novaspace proprietary database.

[4] According to Novaspace estimations.

[5] According to Novaspace estimations.

[6] U.S. General Services Administration, SAM.gov, “Commercial Lunar Payload Services (CLPS) 2.0,” NASA Johnson Space Center, accessed April 21, 2026, https://sam.gov/workspace/contract/opp/952ef3887980411aacd9dee70a370dd9/view.

[7] National Aeronautics and Space Administration (NASA), “Building the Moon base,” PDF, accessed April 20, 2026, https://www.nasa.gov/wp-content/uploads/2026/03/2-building-the-moon-base.pdf.

[8] National Aeronautics and Space Administration (NASA), “Building the Moon base,” PDF, accessed April 20, 2026, https://www.nasa.gov/wp-content/uploads/2026/03/2-building-the-moon-base.pdf.

[9] U.S. General Services Administration, SAM.gov, “Commercial Lunar Payload Services (CLPS) 2.0,” NASA Johnson Space Center, accessed April 21, 2026, https://sam.gov/workspace/contract/opp/952ef3887980411aacd9dee70a370dd9/view.

[10] U.S. General Services Administration, SAM.gov, “Commercial Lunar Payload Services (CLPS) 2.0,” NASA Johnson Space Center, accessed April 21, 2026, https://sam.gov/workspace/contract/opp/952ef3887980411aacd9dee70a370dd9/view.