Satellite constellations are redefiningthe global maritime communications market over the coming decade after shipping operators adopt hybrid approach.

The maritime satellite communication market experienced significant growth in 2023, primarily driven by Starlink’s disruptive entry into the market following the official launch of its maritime service, which has rapidly gained traction and boosted the number of VSAT-equipped vessels.

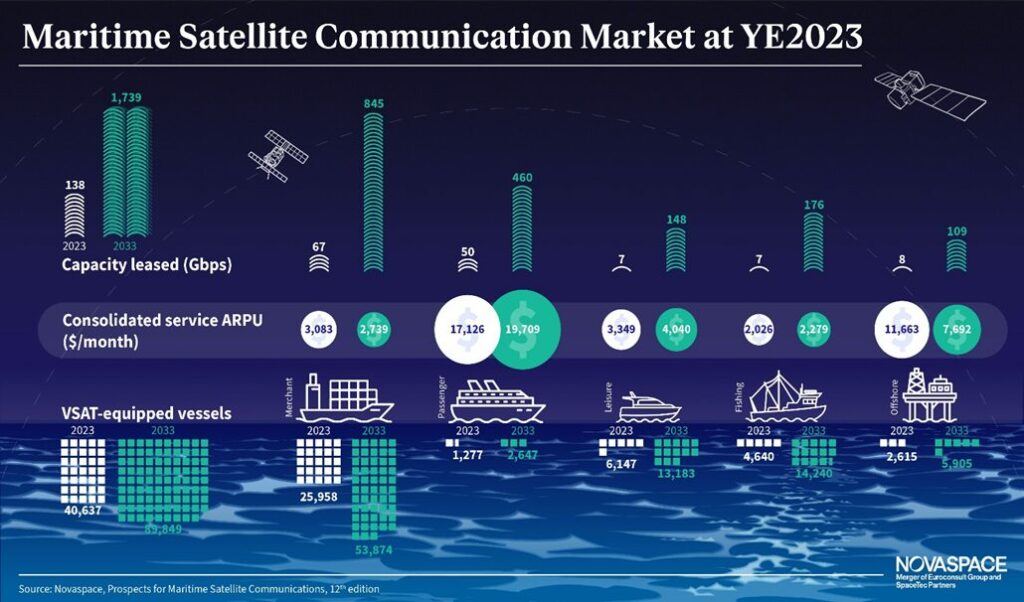

The latest release of Prospects for Maritime Satellite Communications from Novaspace, a merger between Euroconsult and SpaceTec Partners, the leading space consulting and market intelligence firm, reveals the market share of Non-Geostationary Orbit (NGSO) solutions as a primary maritime communications method is expected to surge from 20% in 2023 to 90% by 2033. It reveals the total number of vessels using at least one satellite communication service during 2023 reached 40,600, a number which is projected to more than double in 10 years, reaching approximately 90,000 vessels by 2033.

The Novaspace report also shows that while large vessel operators have been cautious about relying solely on NGSOs for connectivity, they are increasingly adopting a hybrid approach by using existing Geostationary Orbit (GEO) solutions as a companion to NGSO services. This strategy temporarily increased their overall satcom budget in 2023, but costs are anticipated to normalize as the ownership costs of satcom solutions decrease.

Bandwidth usage has doubled in the last year mainly due to Starlink’s entry and is forecasted to grow exponentially from 138 Gbps in 2023 to 1.7 Tbps by 2033, a 13-fold increase. The reliance on GEO capacity as the primary communication means will decline as vessels transition to NGSO for their primary bandwidth needs. Consequently, NGSO capacity’s market share is expected to rise from 66% in 2023 to 96% by 2033.

New-generation NGSO systems will also exert pressure on the current ecosystem, leading to decreased capacity prices. These advanced systems will exponentially increase capacity supply, enabling higher capacity usage and offsetting the price decrease. Operator revenues are projected to grow from just under $620 million in 2023 to approximately $1.14 billion by 2033, with a 6% compound annual growth rate (CAGR) over the decade.

Additionally, service revenues for the maritime market are anticipated to rise from $1.8 billion in 2023 to $3 billion by 2033. This growth is attributed to the increasing number of VSAT-equipped vessels and higher average revenue per user (ARPU) in certain sub-verticals. The service revenue market share generated by NGSOs is expected to climb from 17% in 2023 to 87% by 2033.

“The maritime satcom market continued to be highly dynamic in 2023 with the impact of Starlink’s market disruption was felt across the various sub-segments and expected to continue throughout 2024,” said Vishal Patil, Novaspace consultant and the report’s editor. “While many vessel operators now have first-hand experience with Starlink services, several other suppliers are set to follow, including OneWeb during 2024, which will further accelerate the global adoption of NGSO services.”